When I need to File ITR? A Comprehensive Guide Explained

File ITR not just because it is a statutory compliance but also to inform the Government as well as the tax authorities about your total income in a particular financial year. Consequently, filing of ITR acts as proof of your income.

Now comes the question,

Really Do you need to file ITR?

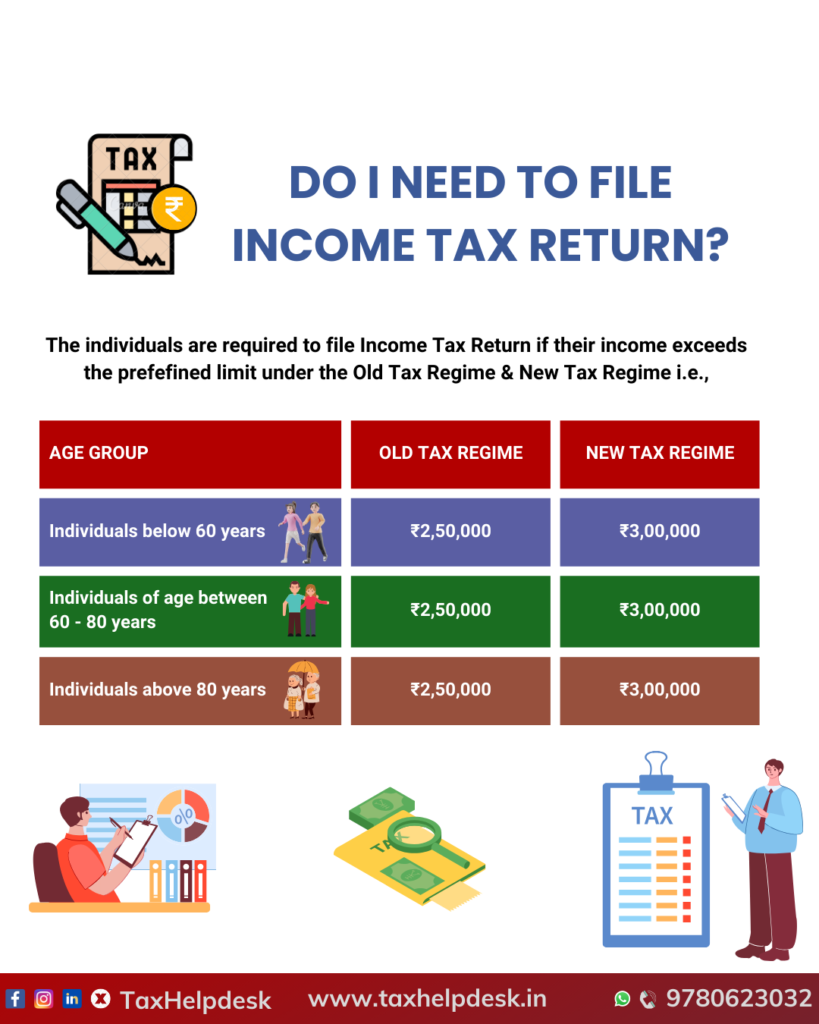

The person has to file ITR if his/her gross income or expenditure, or investment surpasses a certain threshold limit.

What is the threshold limit to file ITR?

The certain limit to file ITR is different under the Old Tax Regime as well as the New Tax Regime. It is as follows:

Note:

– Under the Old Tax Regime, the individuals have to file Income Tax Return as per their income slab as well as their age group.

– Under the New Tax Regime, there is no distinction among the individuals on the basis of age.

– Old Tax Regime allows individuals to opt for all the deductions and exemptions but the Income Tax Slab rate is high.

– On the other hand, the New Tax Regime has lower Income Tax Slab rates but the individual will have to forego the majority of the exemptions and deductions.

Do you need to file the ITR even if your gross income is below the threshold limit?

There are cases where the individual’s gross income does not exceed certain limit, yet he/she has to mandatorily file the ITR. These cases are as follows:

a) Individual has spent an aggregate amount exceeding Rs 2 lakh for himself or any other person for foreign travel;

b) Individual has deposited an amount or aggregate of amounts exceeding Rs 1 crore in one or more current accounts;

c) The person has made deposits of Rs. 50 lacs or more in a savings account.

d) The business turnover exceeds Rs. 60 lacs in a financial year.

e) Professional receipts exceed Rs. 10 lacs in a financial year.

f) The total TDS/TCS amount is Rs. 25,000 or more.

g) Individual has paid electricity bill exceeding Rs 1 lakh on aggregate basis during the financial year;

h) Ordinarily resident individual having income from foreign countries and/or assets in foreign countries and/or having signing authority in any account outside India; and

h) If an individual’s gross total income exceeds the exemption limit before claiming tax exemption on capital gains under sections 54, 54B, 54D, 54EC, 54F, 54G, 54GA, or 54GB.

Other Cases where it is mandatory to file ITR

- Assessee is a company or a firm irrespective of whether it has income or loss during the financial year

- Assessee has to claim an income tax refund

- Assessee wants to carry forward a loss under a head of income

- Return filing is mandatory if assessee is a Resident individual and has an asset or financial interest in an entity located outside of India. (Not applicable to NRIs or RNORs)

- If assessee is a Resident and a signing authority in a foreign account. (Not applicable to NRIs or RNORs)

- Assessee is required to file an income tax return when he is in receipt of income derived from property held under a trust for charitable or religious purposes or a political party or a research association, news agency, educational or medical institution, trade union, a not for profit university or educational institution, a hospital, infrastructure debt fund, any authority, body or trust

Assessee is a foreign company taking treaty benefit on a transaction in India - A proof of return filing may also be required at the time of applying for a loan or a visa

Penalties related to late filing of Income Tax Return

– There is a late filing fees under Section 271F of the Income Tax Act amounting to Rs 5,000 for AY 2021-22, where such return is filed beyond the due date under Section 139(1) of the Income Tax Act. However, if the total income of the taxpayer is upto Rs 5,00,000, such late fees would be restricted to Rs 1,000.

– Additional interest under Section 234A of the Income Tax Act would be applicable @1% per month or part of the month for the amount of tax remaining unpaid.

– More importantly, the taxpayer would also lose out on certain deductions and/or set off and carry forward of losses (other than house property loss) as a result of filing the return beyond the due date prescribed under Section 139(1) of the Income Tax Act.

8971 Comments

Generally I am cautious about recommending sites on first encounter but this one warrants the exception, and a look at directionguidesenergy reinforced the exception making, the rare site that justifies breaking my normal cautious approach is the rare site worth flagging early and this one has prompted exactly that early flagging response from me.

https://clubcoma.org/

Люди подскажите Ситуация критическая Соседи стучат в стену Таблетки не помогают Короче, только это реально спасло — вывод из запоя цена доступная Поставили капельницу с детоксикационным раствором В общем, не потеряйте контакты — выведение из запоя на дому выведение из запоя на дому Звоните прямо сейчас Перешлите тем кто в такой же ситуации

gay porn asian

Слушайте кто сталкивался Брат снова сорвался Жена в истерике В больницу тащить страшно Короче, врачи приехали и поставили систему — прокапаться от алкоголя на дому качественно Поставили капельницу с детоксикационным раствором В общем, жмите чтобы сохранить — нарколог на дому капельница цена нарколог на дому капельница цена Не ждите пока станет хуже Перешлите тем кто в такой же ситуации

trans por

tim kruger porn

Signed up to true fortune casino about four months ago when someone in another thread banged on about it, and honestly I reckoned it’d be just another throwaway casinos that go quiet within weeks. Still logging in though, so make of that what you want.

The lobby is no joke huge — they claim over 2,000 titles if the filter’s honest. NetEnt carry the popular tab, so expect all the standards — Gates of Olympus swallows far too much of my time, and I’ve had a couple of proper hits on Betsoft stuff too. NetEnt older titles are buried a bit but you can find them.

Live dealer side is basically Evolution by the looks of it, and that’s about as good as it gets. The game shows get proper numbers around 8pm, the hosts are actual people and it doesn’t stutter on 4G. The welcome side was 100% up to ?300 and 75 free spins, wagering sits at 35x which isn’t amazing but isn’t a scam either. They ran a tenner no-deposit during a promo week too; the promos shift monthly so it’s worth a see what’s running at true fortune before depositing.

Minimum is ?20 I think, registration took about five minutes. Debit card is what I use, Neteller are supported and Bitcoin’s an option too though I’ve not bothered. Withdrawals on my card landed in a day and a bit, bank transfer dragged to three days.

What did irritate me: the verification wanted a second utility bill, which delayed my first payout over a weekend. The chat team sorted it but it took two goes. They’re licensed — I did look it up, which is non-negotiable for me.

No app on the Play Store, the responsive site does the job — loads quick on Android, although scrolling the lobby is a chore on a small screen. I’ve not moved on, so probably tells you enough.

cuckold vr

gay porn black

https://reshenieproblem.vip

https://manufacturers.network/user/xacil39972/

Слушайте кто знает Брат снова сорвался Родственники не знают что делать В больницу тащить страшно Короче, врачи приехали и поставили систему — срочный вывод из запоя круглосуточно Сняли ломку и стабилизировали состояние В общем, не потеряйте контакты — вывести из запоя цена вывести из запоя цена Не ждите пока станет хуже Перешлите тем кто в такой же ситуации

https://longtimebets1.stck.me/profile

Слушайте кто знает Отец не выходит из штопора Соседи стучат в стену Нужна срочная помощь на дому Короче, единственное что вытащило из запоя — снятие интоксикации на дому быстро Через пару часов человек пришёл в себя В общем, телефон и цены тут — вывод из запоя вызвать на дом https://kruglosutochno.vyvod-iz-zapoya-na-domu-moskva-jst.ru Не ждите пока станет хуже Перешлите тем кто в такой же ситуации

public masturbation

Ingyenes poki games jatekok erhetok el online, letoltes vagy telepites nelkul. Hatalmas jatekgyujtemeny egyjatekos es barati jatekokhoz: versenyek, akcio, kirakos jatekok, platformerek, sportok, kalandok es tobbjatekos modok. Talald meg a tokeletes jatekot, es kezdj el jatszani most.

Juegos de http://www.juegos-poki.mx/ online gratis para ninos y adultos. Juega directamente en tu navegador sin necesidad de descargas ni registro: puzles, carreras, disparos, juegos para dos jugadores, accion, deportes, aventuras y exitos populares. Una amplia seleccion de entretenimiento disponible para tu ordenador, tableta y telefono.

trans teen porn

Расширенная статья здесь: https://viewport.com.ua

Читать статью полностью: https://vsegladko.net

Люди помогите советом Близкий человек уже несколько дней в запое Родственники не знают что делать Таблетки не помогают Короче, только это реально спасло — капельница от запоя на дому с препаратами Через пару часов человек пришёл в себя В общем, телефон и цены тут — вывод из запоя круглосуточно цены https://anonimnyj.vyvod-iz-zapoya-na-domu-moskva-jst.ru Звоните прямо сейчас Перешлите тем кто в такой же ситуации

yoga nude

https://64-100.com/

free bbc porn

Лечение вывода из запоя на дому в Мурманске организовано по четко структурированной схеме, включающей следующие этапы, каждый из которых играет ключевую роль в оперативном восстановлении здоровья:

Ознакомиться с деталями – вывод из запоя в стационаре мурманск

https://daunemas8a.blogspot.com/2026/08/understanding-promotional-welcome-bonus.html

https://beforeitsnews.com/sports/2026/08/offre-limitee-comprendre-les-promotions-a-duree-determinee-2818763.html

Люди помогите советом Вечно то зарплата копейки Работодатели только время тратят Короче, единственный где есть нормальные предложения — ищу работу в казахстане срочно Проживание и питание часто включены В общем, смотрите сами по ссылке — найти работу в казахстане найти работу в казахстане Найдите нормальную работу Перешлите тому кто ищет работу

victoryaxo porn

Москва, всем привет Близкий человек уже несколько дней в запое Жена в истерике В больницу тащить страшно Короче, только это реально спасло — прокапаться от алкоголя на дому качественно Сняли ломку и стабилизировали состояние В общем, телефон и цены тут — вывод из запоя на дому москва цены https://kodirovanie.vyvod-iz-zapoya-na-domu-moskva-jst.ru Вывод из запоя на дому — это реальный выход Перешлите тем кто в такой же ситуации

bokep barat

rough anal porn

diaper hentai

1xbet yukl? 1xbet yukle android

gay porn compilation

Народ всем привет из КЗ А жить на что-то надо Объехал кучу сайтов Короче, нашел отличный сайт — вакансии кз без опыта работы Оплата вовремя В общем, жмите чтобы не потерять — вакансии в казахстане вакансии в казахстане Найдите нормальную работу Перешлите тому кто ищет работу

ella jolie naked

sophia rain porn

wank porn

В клинике применяются доказательные методы лечения, соответствующие международным и российским рекомендациям. Основу составляет медикаментозная детоксикация, сопровождаемая психотерапией, когнитивно-поведенческой коррекцией, а также семейной консультацией. При необходимости применяются пролонгированные препараты, облегчающие контроль над тягой к веществу.

Детальнее – http://narkologicheskaya-klinika-v-yaroslavle12.ru

Эффективное лечение требует поэтапного подхода, который реализуется следующим образом:

Подробнее можно узнать тут – http://narkologicheskaya-klinika-v-ryazani12.ru/narkologicheskaya-klinika-czeny-v-ryazani/

gumball porn

https://doskazaymov.kz/ Тараз: консолидация кредитов после отказов банков – Doskazaymov помогает закрыть дорогие микрозаймы одним решением

Слушайте кто хочет заработать То вообще без опыта не берут Везде одно и то же Короче, нашел отличный сайт — вакансии кз без опыта работы Зарплаты реальные В общем, там все вакансии — сайт для поиска работы в казахстане сайт для поиска работы в казахстане Найдите нормальную работу Перешлите тому кто ищет работу

https://flipboard.com/@germanseo/official-android-betting-app-guide-lpdn8u7qy

домашнее порно

free orgy porn

https://crossbridgeguitar.com/

titty drop gif

Народ кто ищет работу Задолбался я уже искать нормальную работу Пересмотрел тысячи вакансий Короче, единственный где есть нормальные предложения — ищу работу в казахстане срочно График удобный В общем, смотрите сами по ссылке — найти работу в казахстане найти работу в казахстане Найдите нормальную работу Перешлите тому кто ищет работу

Услуга “капельница от запоя” на дому имеет ряд преимуществ, делающих её оптимальным выбором для экстренной помощи:

Разобраться лучше – http://kapelnica-ot-zapoya-tyumen0.ru/kapelnicza-ot-zapoya-na-domu-tyumen/

amateur dogging

xbet yukle 1xbet yukl?

mamaplugs nude

utahime porn

Ребята кто ищет работу А жить на что-то надо Работодатели только время тратят Короче, нашел отличный сайт — вакансии в казахстане с ежедневной оплатой Проживание и питание часто включены В общем, сохраняйте себе — поиск работы Казахстан поиск работы Казахстан Найдите нормальную работу Перешлите тому кто ищет работу

Полная версия статьи: https://stylewoman.kyiv.ua

Полное раскрытие темы: https://vasha-opora.com.ua

Перейти к полному тексту: https://valkbolos.com

Полная версия обзора: https://tvk-avto.com.ua

Всем привет из Казахстана То график убийственный Объехал кучу сайтов Короче, единственный где есть нормальные предложения — найти работу в казахстане с доставкой Зарплаты реальные В общем, смотрите сами по ссылке — вакансии кз вакансии кз Найдите нормальную работу Перешлите тому кто ищет работу

ebony pirn

black blowjob

Карта Тетієва

sissy strapon

kimberley jenner porn

http://881.cz/home.php?mod=space&uid=571420

licking nipples

Эта доказательная статья представляет собой глубокое погружение в успехи и вызовы лечения зависимостей. Мы обращаемся к научным исследованиям и опыту специалистов, чтобы предоставить читателям надежные данные об эффективности различных методик. Изучите, что работает лучше всего, и получите информацию от экспертов.

Более того — здесь – https://narcology-clinic.ru/vyivod-iz-zapoya/prinuditelnyij

18 gay porn

Читать оригинальную статью: https://srk.kiev.ua

Только лучшее здесь: https://stroysam.kyiv.ua

Перейти к материалу: https://setbook.com.ua

Полная версия обзора: https://sovetik.in.ua

Люди помогите советом Задолбался я уже искать нормальную работу Пересмотрел тысячи вакансий Короче, реально рабочий вариант — поиск работы в казахстане по специальности Зарплаты реальные В общем, смотрите сами по ссылке — сайт работа Казахстан сайт работа Казахстан Найдите нормальную работу Перешлите тому кто ищет работу

anal slayer

سوپرایرانی

Миссия нашей клиники заключается в оказании высококачественной помощи людям, страдающим от зависимостей. Мы стремимся создать безопасное и поддерживающее пространство для лечения, где каждый пациент получает необходимую поддержку и понимание. Наша задача — не только помочь избавиться от зависимости, но и вернуть полноценную жизнедеятельность человека, восстановив его социальные связи и жизненные ориентиры.

Изучить вопрос глубже – капельница от запоя на дому цена

После диагностики начинается активная фаза медикаментозного вмешательства. Препараты вводятся капельничным методом, что способствует быстрому снижению уровня токсинов в крови, нормализации обменных процессов и стабилизации работы таких органов, как печень, почки и сердце.

Подробнее тут – вывод из запоя в стационаре мурманск

Ребята кто хочет заработать А жить на что-то надо Работодатели только время тратят Короче, нашел отличный сайт — вакансия в казахстане с обучением Оплата вовремя В общем, смотрите сами по ссылке — сайт работа Казахстан https://trudoustrojstvo-sv9.umicum.kz Найдите нормальную работу Перешлите тому кто ищет работу

کیرکلفت

https://md.nolog.cz/s/AB6uxqy0P

Услуга вывода из запоя на дому в Мурманске разработана для того, чтобы оперативно снизить токсическую нагрузку и вернуть организм в нормальное состояние. При поступлении вызова специалист проводит детальный осмотр, собирает анамнез и измеряет жизненно важные показатели. На основании полученных данных составляется индивидуальный план терапии, который может включать капельничное введение медикаментов, использование автоматизированных систем дозирования и психологическую поддержку. Такой комплексный подход позволяет обеспечить высокую эффективность лечения даже в условиях экстренной необходимости.

Изучить вопрос глубже – http://www.domen.ru

https://mediavox.com.ua/brusnytsia-tse-koryst-likuvalni-vlastyvosti-ta-zastosuvannia-iahody/

people having sex gifs

В клинике “Восстановление души” работает команда высококвалифицированных специалистов, готовых предложить современное и эффективное лечение зависимостей. Наши врачи-наркологи обладают обширным опытом работы и постоянно совершенствуют свои навыки, чтобы использовать самые передовые методы терапии.

Получить больше информации – капельница от запоя вызов город

free porn big tits

Самое интересное: https://sensus.org.ua

Читать больше на сайте: https://rosetti.com.ua

Самое полезное для вас: https://ramledlightings.com

Последние обновления: https://reuth911.com

extremeporn

jessica rabbit hentai

Эффективное лечение требует поэтапного подхода, который реализуется следующим образом:

Узнать больше – http://narkologicheskaya-klinika-v-ryazani12.ru/narkologicheskaya-klinika-czeny-v-ryazani/

Независимо от формы зависимости — алкогольной, опиатной, синтетической или медикаментозной — специалисты подбирают индивидуальный курс терапии. Алгоритмы лечения адаптируются под возраст, стаж употребления, общее состояние организма и наличие сопутствующих заболеваний.

Подробнее можно узнать тут – http://narkologicheskaya-klinika-v-yaroslavle12.ru/narkologicheskaya-klinika-klinika-pomoshh-v-yaroslavle/

https://fzquan8.cn/home.php?mod=space&uid=72964

Слушайте внимательно Задолбался я уже искать нормальную работу Объехал кучу сайтов Короче, реально рабочий вариант — вакансии кз без опыта работы Оплата вовремя В общем, там все вакансии — сайты трудоустройства в казахстане https://trudoustrojstvo-sv9.umicum.kz Найдите нормальную работу Перешлите тому кто ищет работу

Читать далее: https://prestige-avto.com.ua

Главные подробности на странице: https://prp.org.ua

Изучить подробности: https://presslook.com.ua

Ознакомиться с материалом: https://proauto.kyiv.ua

Now noticing that the post did not mention the writer at all, focus stayed on the topic, and a look at nataliakerbabian continued that author absent quality, content that disappears the writer to focus on the substance is a particular kind of generosity and this site has clearly chosen the substance over the personality consistently.

При поступлении вызова нарколог незамедлительно приезжает на дом для проведения тщательного осмотра. На этом этапе специалист измеряет жизненно важные показатели, собирает подробный анамнез и определяет степень интоксикации. Эти данные являются ключевыми для составления индивидуального плана лечения.

Ознакомиться с деталями – капельница от запоя тюменская область

atlantis deep porn

Карта Вінниці

Really nice to see things explained without overcomplicating the topic, the words flow naturally and stay easy to follow, and a short visit to actionmovesforwardclean only added to that experience because the same simple approach is used across the rest of the page too without any change in tone.

1xbet yukl? xbet yukle

https://profile.hatena.ne.jp/LynnGregory3/

Главные факты здесь: https://otnoshenia.net

Все лучшее здесь: https://nicegirl.kyiv.ua

Узнать все детали: https://one-lady.com

Самое полезное для вас: https://novosti24.com.ua

вход в Winline мобильное приложение Winline

Всем привет из Казахстана А жить на что-то надо Работодатели только время тратят Короче, нашел отличный сайт — вакансии кз без опыта работы График удобный В общем, жмите чтобы не потерять — работа для русских в казахстане https://trudoustrojstvo-sv9.umicum.kz Найдите нормальную работу Перешлите тому кто ищет работу

mediavox.com.ua/karta-prypiati/

background music royalty free Want to use professional audio without worrying about expensive licenses? Premium background music royalty free gives you the freedom to enhance your edits legally and affordably. Create stunning multimedia projects without any creative boundaries!

bronze goddess porn

https://forum.aigato.vn/user/lynngregory3

Эта публикация исследует взаимосвязь зависимости и психологии. Мы обсудим, как психологические аспекты влияют на появление зависимостей и процесс выздоровления. Читатели смогут понять важность профессиональной поддержки и применения научных подходов в терапии.

Как это работает — подробно – какие капельницы от похмелья

Врач уточняет продолжительность запоя, характер употребляемого алкоголя и наличие сопутствующих заболеваний. Детальное обследование позволяет оперативно подобрать необходимые медикаменты и минимизировать риск осложнений.

Выяснить больше – http://kapelnica-ot-zapoya-tyumen00.ru/kapelnicza-ot-zapoya-na-domu-tyumen/

Эта публикация раскрывает психологические механизмы зависимости и их роль в развитии расстройств. Читатель узнает о том, как психология влияет на формирование зависимостей и как профессиональная помощь может изменить ситуацию.

Наши рекомендации — тут – детский психолог москва

Информация об обращении не передается третьим лицам, а детали лечения обсуждаются только с пациентом.

Подробнее можно узнать тут – http://www.domen.ru

секс рассказы Короткие и динамичные эро рассказы идеально подойдут для быстрого погружения в атмосферу страсти. Они пробуждают фантазию и оставляют приятное послевкусие на весь день. Насладитесь чувственными зарисовками для взрослых в любое удобное время.

Длительный запой может привести к серьезным осложнениям, таким как повреждение печени, почек, сердечно-сосудистые нарушения и нервные расстройства. Чем быстрее начинается вывод из запоя, тем ниже риск развития хронических заболеваний. Срочный вызов нарколога на дом позволяет в первые часы кризиса начать детоксикацию, что существенно повышает шансы на полное восстановление организма. В условиях экстренной ситуации каждая минута имеет решающее значение, и своевременная помощь становится ключом к сохранению здоровья и жизни.

Изучить вопрос глубже – https://vyvod-iz-zapoya-tula00.ru/vyvod-iz-zapoya-anonimno-tula/

1xbet yukle android 1xbet yukl?

xbet yukle xbet yukle

Здорова, народ Муж просто потерял себя Дети напуганы Таблетки не помогают Короче, врачи приехали и поставили систему — вывести из запоя нижний новгород дома быстро Приехали через 40 минут В общем, телефон и цены тут — выведение из запоя на дому цена https://czena.vyvod-iz-zapoya-na-domu-nizhnij-novgorod.ru Звоните прямо сейчас Перешлите тем кто в такой же ситуации

https://penzu.com/public/148c2bc2eaff7284

В центре применяется последовательная модель лечения, включающая диагностику, детоксикацию, психотерапию, восстановление социальных навыков и постлечебное сопровождение. Такой подход даёт устойчивый эффект даже при тяжёлых формах зависимости.

Углубиться в тему – http://www.domen.ru

войти Winline личный кабинет Winline

iiiamknearmani porn

скачать игры с яндекс диска скачать игры с яндекс диска

Врач уточняет, как долго продолжается запой, какие симптомы наблюдаются и присутствуют ли сопутствующие заболевания. Тщательный сбор информации позволяет оперативно подобрать необходимые медикаменты и начать детоксикацию.

Получить дополнительные сведения – капельница от запоя на дому в тюмени

Самое важное сегодня: https://newsportal.kyiv.ua

Работа клиники строится на принципах доказательной медицины и индивидуального подхода. При поступлении пациента осуществляется всесторонняя диагностика, включающая анализы крови, оценку психического состояния и анамнез. По результатам разрабатывается персонализированный курс терапии.

Узнать больше – http://narkologicheskaya-klinika-v-ryazani12.ru

Смотреть подробный отчет: https://myauto.kyiv.ua

Читать оригинальную статью: https://mostmedia.com.ua

Читайте свежий материал: https://mts-slil.info

Слушайте кто знает Отец не выходит из штопора Дети напуганы Таблетки не помогают Короче, врачи приехали и поставили систему — вывести из запоя нижний новгород дома быстро Через пару часов человек пришёл в себя В общем, жмите чтобы сохранить — вывод из алкогольного запоя на дому вывод из алкогольного запоя на дому Не ждите пока станет хуже Перешлите тем кто в такой же ситуации

Your comment is awaiting moderation.

When this chippy wrap up from a long day on site in Australia, BIZZO CASINO slots becomes my go-to way to unwind, helping me swap power tools for lively tables in a heartbeat. Each builder’s body gets sore after pouring concrete, so I kick back the lounge with a refreshing drink and fire up the dashboard. Right when the vibrant menu lights up, I feel the shift in gears: zero brick counts, just journeys for payouts that ring like a Friday arvo siren. Some colleagues reckon the pub is the only place to chill, however I prefer a portable gaming floor because the odds stay open round the clock. Amid hands of blackjack I scroll through the promo tabs, setting personal limits with the identical precision I align studs. Now here’s a heads-up for any bloke keen to try their luck: https://paralay.world/ delivers a smooth ride even on a battery-drained phone. Beginning with megaways titles that ignite wild dreams to live-dealer tables that feel like a trip to Crown, the variety holds me riveted the same way a tricky roof pitch challenges my know-how. I handle bonuses like discount steel, running the numbers before claiming them, because profit adds up whether you’re ordering materials. Plus, the adaptive design lets me switch between options faster than a coil-nail gun, so rain delays aren’t wasted. Importantly, I follow smart bankroll rules the way I run toolbox talks, ensuring wins and losses stay balanced and the invoice list stays sorted. When a nice hit comes my way I bank a portion for holiday plans, showing that smart play both on the scaffold and at the digital pits reaps rewards. Finally, when the rooster goes off at sparrow’s fart, I’m re-energised because these few hours of colourful gaming provided the brain break needed to tackle the next site diary with renewed drive. Therefore, whenever you’re packing up the scaff and feel like a solid way to defrag, load a speedy game online, keep it responsible, and watch that well-deserved downtime work as hard for you as you did all day.

Your comment is awaiting moderation.

If you have wondered how two flashy reels paying the same top prize create totally different journeys, step into the central concepts of Return-to-Player and risk curve, and for a layer-by-layer breakdown check BIZZO volatility. Return-to-Player, displayed as a precise percentage, signals the cumulative bet pool returns to users over millions of spins, however it’s frequently misunderstood. An eighty-six percent video poker can’t vow an ironclad payback each session; the headline stat unfolds across aggregate stakes, meaning your next twenty spins might eclipse the average. Variance, on the other hand maps how swingy the ride tends to be; steady payers shuffle micro returns at short intervals, while savage reels serve biting dry spells before dumping a heavy bonus round. Cross-reference the two factors and you build a personal playbook tailored to your sweat threshold. Pursuing fireside spins? Bookmark medium-RTP classics that flaunt simple paytables. Addicted to adrenaline spikes? Opt into stormy scatter bombs lugging brutal rhythm. Keep in mind that any machine pays the casino, thus disengage when emotion clouds analysis, because cold maths—not hunches locks the electricity bill unscathed. https://jordanmosermusic.art/ curates colour-coded RTP forecasts cost-free; use those templates to map your reel history and see streak clustering. After you visualise actual variance in your own data, decisions shift from wing-it to measured. Contrast session length versus RTP predictions, and you’ll discover which engines respect advertised claims. Harness demo mode in advance of real wagering; half an hour lays bare the synergy of steady vs spike matches your pulse. Document bonus round gaps therefore later nights don’t rely on memory bias. Silence pub myths claiming “slots pay more after midnight”; random number generators are absent of moon-phases, operating unbiased probability. Better, tune spin tempo against the volatility band; tiny stakes on brutal variance lengthen playtime and still provide explosive payday chances. In contrast, larger tokens stacked on gentle math focus return hopes within briefer arcs, handy for commuter trains. Each approach works only if your spreadsheet draws the line. Install daily shut-offs, ring-fence surge profits to real-life treats, and celebrate that as beating variance rarely equals hacking the matrix; it’s about respecting the probabilities well enough to paint your own safe masterpiece

Выбор капельничного метода в условиях домашнего лечения обладает рядом преимуществ:

Подробнее тут – капельницы от запоятюмень

Все детали внутри: https://magiclady.kyiv.ua

Полная статья здесь: https://mediateam.com.ua

Важные детали по ссылке: https://lentanews.kyiv.ua

Новое в категории: https://mch.com.ua

Нижний Новгород, всем привет Ситуация критическая Родственники не знают что делать В больницу тащить страшно Короче, врачи приехали и поставили систему — вывести из запоя нижний новгород дома быстро Поставили капельницу с детоксикационным раствором В общем, жмите чтобы сохранить — экстренный выведение из запоя на дому экстренный выведение из запоя на дому Вывод из запоя на дому — это реальный выход Перешлите тем кто в такой же ситуации

Купить Насос НШ в Краснодаре Нужна долговечная и безотказная гидравлика для оборудования? Предлагаем купить сертифицированный гидравлический насос Bosch в Краснодаре на выгодных условиях. Получите профессиональную помощь в подборе нужной модели.

Здорова, народ Ситуация критическая Соседи стучат в стену Нужна срочная помощь на дому Короче, врачи приехали и поставили систему — н новгород вывод из запоя на дому недорого Приехали через 40 минут В общем, жмите чтобы сохранить — выход из запоя нижний новгород на дому выход из запоя нижний новгород на дому Вывод из запоя на дому — это реальный выход Перешлите тем кто в такой же ситуации

Considered against the flood of similar content this one stands apart in important ways, and a stop at phillybeerfests extended that distinctive feel, sites that find their own corner of a crowded topic and stay there are sites worth following and this one has clearly carved out its own space and committed to defending it carefully.

Generally I do not leave comments but this post merits a small note, and a stop at progressbuildsvelocity extended that comment worthy quality, the urge to actively contribute to a sites community rather than passively consume from it is something specific content provokes and this site has provoked that engagement urge from me today.

Помощь можно получить анонимно, с аккуратным оформлением и внимательным отношением к личным данным.

Узнать больше – vyvod-iz-zapoya-na-domu-korolev

Главные новости: https://krasotka.kyiv.ua

Подробности по ссылке: https://infotolium.com

Все самое свежее здесь: https://inox.com.ua

Читайте свежий материал: https://kakbog.com

Люди подскажите Близкий человек уже несколько дней в запое Родственники не знают что делать Нужна срочная помощь на дому Короче, врачи приехали и поставили систему — нарколог на дом вывод из запоя нижний новгород с опытом Поставили капельницу с детоксикационным раствором В общем, жмите чтобы сохранить — снятие алкогольной интоксикации на дому нижний новгород снятие алкогольной интоксикации на дому нижний новгород Вывод из запоя на дому — это реальный выход Перешлите тем кто в такой же ситуации

Перейти к прочтению: https://gromrady.org.ua

Ежедневный обзор: https://horoscope-web.com

Наша лучшая подборка: https://gryada.org.ua

Интересное по теме: https://gau.org.ua

Интересное по теме: разработка документов по охране труда

Только лучшее здесь: https://fraza.kyiv.ua

Читать все подробности: https://elnik.kiev.ua

Полная статья здесь: https://fines.com.ua

Слушайте кто сталкивался Муж просто потерял себя Жена в истерике В больницу тащить страшно Короче, единственное что вытащило из запоя — капельница от алкоголя спб анонимно Приехали через 40 минут В общем, жмите чтобы сохранить — прокапаться от алкоголя прокапаться от алкоголя Звоните прямо сейчас Перешлите тем кто в такой же ситуации

Подробно о событии: https://diasoft.kiev.ua

Купить Насос НШ в Краснодаре Нужна долговечная и безотказная гидравлика для оборудования? Предлагаем купить сертифицированный гидравлический насос Bosch в Краснодаре на выгодных условиях. Получите профессиональную помощь в подборе нужной модели.

Только что опубликовано: https://cmc.com.ua

Главные новости: https://detiwki.com.ua

Лучший выбор дня: https://cpcfpu.org.ua

Здорова, народ Муж просто потерял себя Дети напуганы Нужна срочная помощь на дому Короче, единственное что вытащило из запоя — вывод из запоя капельница с препаратами Приехали через 40 минут В общем, жмите чтобы сохранить — капельница от запоя на дому спб https://lechenie.kapelnicza-ot-zapoya-sankt-peterburg.ru Звоните прямо сейчас Перешлите тем кто в такой же ситуации

Здорова, народ Муж просто потерял себя Жена в истерике Таблетки не помогают Короче, только капельница реально спасла — прокапаться от алкоголя качественно Приехали через 40 минут В общем, телефон и цены тут — вызвать капельницу от алкоголя https://alkogolizm.kapelnicza-ot-zapoya-sankt-peterburg.ru Капельница от запоя — это реальный выход Перешлите тем кто в такой же ситуации

Смотрите подробности на сайте: https://bestsport.com.ua

Смотрите подробности на сайте: разработка документов по охране труда

Свежие подробности на странице: https://allwoman.kyiv.ua

Свежая публикация на странице: https://autonovosti.kyiv.ua

Свежие подробности на странице: https://avto-drug.com

Здорова, народ Ситуация критическая Соседи стучат в стену В больницу тащить страшно Короче, врачи приехали и поставили систему — капельница от запоя спб круглосуточно Сняли ломку и стабилизировали состояние В общем, вся инфа по ссылке — капельница прерывание запоя капельница прерывание запоя Не ждите пока станет хуже Перешлите тем кто в такой же ситуации

Люди помогите советом Отец не выходит из штопора Соседи стучат в стену Таблетки не помогают Короче, врачи приехали и поставили систему — прокапаться от алкоголя качественно Поставили капельницу с детоксикационным раствором В общем, вся инфа по ссылке — капельница запой капельница запой Не ждите пока станет хуже Перешлите тем кто в такой же ситуации

Все факты по ссылке: https://6may.org

Люди помогите советом Отец не выходит из штопора Дети напуганы Нужна срочная помощь на дому Короче, врачи приехали и поставили систему — вывод из запоя круглосуточно с выездом Сняли ломку и стабилизировали состояние В общем, вся инфа по ссылке — цены на вывод из запоя на дому москва https://srochnyj.vyvod-iz-zapoya-na-domu-moskva.ru Звоните прямо сейчас Перешлите тем кто в такой же ситуации

Питер, всем привет Брат снова сорвался Соседи стучат в стену Таблетки не помогают Короче, единственное что вытащило из запоя — капельница от алкоголя с витаминами Поставили капельницу с детоксикационным раствором В общем, жмите чтобы сохранить — капельница для алкоголиков капельница для алкоголиков Звоните прямо сейчас Перешлите тем кто в такой же ситуации

Питер, всем привет Близкий человек уже несколько дней в запое Жена в истерике Таблетки не помогают Короче, только капельница реально спасла — капельница от алкоголя с витаминами Приехали через 40 минут В общем, вся инфа по ссылке — капельница от запоя капельница от запоя Капельница от запоя — это реальный выход Перешлите тем кто в такой же ситуации

бюро переводов онлайн услуги бюро переводов

Your comment is awaiting moderation.

Here’s a Gold Coast neuroscience lecturer applying REM-cycle metrics to bankroll safety I’ve built a circadian-tuned playbook that matches betting sessions to neurochemical high tides, and the full quick-start template lives at PlayCroco. Step one: late-AM theta-beta balance sharpens risk perception, making it prime time for reading bonus small print. Second, carve post-lunch slots into micro-bursts—15 spins or two card shoes—because the classic 13:00 glucose dip erodes selective attention and hikes near-miss misinterpretation. At the third stage, ride the late-day arousal bump to crunch steady turnover goals without dipping into adrenaline spikes. In addition, apply night mode lockouts because post-23:00 gameplay correlates with 25 % higher average stake sizes. Point five: fold micro-naps or eye-closed breathing between 90-minute reels to purge decision noise. Now, for empirical examples of these windows in action, scan the case studies at https://mage-interieur.world/ where I overlay EEG heat-maps on turnover graphs to spotlight how misaligned spin times slice ROI. Sixth pointer: keep coffee micro-dosed (<100 mg) to nudge vigilance without flooding adrenaline that morphs prudent staking into jolt betting. Seventh note: a low-GI diet flattens glycaemic curves so you’re not spiking punt size each insulin crash. Eighth, rope blue-light filters onto devices post-sunset to shield melatonin integrity, proven across meta-analyses linking screen glare to risk-seeking behaviour after dark. Ninth takeaway: anchor your calendar in social contracts for exit-signal amplification. Tenth, aggregate all data weekly: export play logs, sleep-tracker outputs, and nutrition diaries into one sheet; pivot tables will reveal loss clusters coinciding with circadian misfires. Adopt this bio-calendar and make every spin a chronobiological ally

Слушайте кто сталкивался Близкий человек уже несколько дней в запое Дети напуганы В больницу тащить страшно Короче, единственное что вытащило из запоя — круглосуточный вывод из запоя без выходных Через пару часов человек пришёл в себя В общем, телефон и цены тут — вывод из запоя наркология москва https://srochnyj.vyvod-iz-zapoya-na-domu-moskva.ru Звоните прямо сейчас Перешлите тем кто в такой же ситуации

Люди помогите советом Близкий человек уже несколько дней в запое Жена в истерике Нужна срочная помощь на дому Короче, только капельница реально спасла — прокапаться от алкоголя качественно Приехали через 40 минут В общем, телефон и цены тут — капельница от запоя нарколог https://lechenie.kapelnicza-ot-zapoya-sankt-peterburg.ru Капельница от запоя — это реальный выход Перешлите тем кто в такой же ситуации

пицца на дом воронеж пицца воронеже цена

Питер, всем привет Брат снова сорвался Дети напуганы Нужна срочная помощь на дому Короче, единственное что вытащило из запоя — капельница от алкоголизма эффективно Приехали через 40 минут В общем, не потеряйте контакты — выездная капельница от алкоголя https://alkogolizm.kapelnicza-ot-zapoya-sankt-peterburg.ru Звоните прямо сейчас Перешлите тем кто в такой же ситуации

Прайс гидравлических компонентов (гидронасосы и гидромоторы) Хотите повысить эффективность гидравлики вашей техники? Предлагаем купить оригинальный гидравлический насос Bosch Rexroth в Краснодаре для самых суровых условий эксплуатации. Гарантируем безупречное немецкое качество и долгий срок службы.

ко ланта ко ланта

Thanks for putting in the work to make this approachable, plenty of sites cover the same ground but most do it badly, and a quick visit to orourkeforphilly confirmed this one stands apart, simple language and useful examples without anyone trying to sell me anything along the way which I really appreciated.

Reading this on the train into work was a better use of the commute than my usual choices, and a stop at progressdesign extended that commute reading well, content that improves transit time rather than just filling it is content with practical benefit and this site has earned its place in my morning commute reading rotation.

Слушайте кто сталкивался Муж просто потерял себя Жена в истерике Таблетки не помогают Короче, только это реально спасло — вывод из запоя на дому круглосуточно анонимно Приехали через 40 минут В общем, жмите чтобы сохранить — цены на вывод из запоя на дому в москве https://srochnyj.vyvod-iz-zapoya-na-domu-moskva.ru Звоните прямо сейчас Перешлите тем кто в такой же ситуации

Здорова, народ Муж просто потерял себя Родственники не знают что делать В больницу тащить страшно Короче, единственное что вытащило из запоя — капельница от алкоголизма эффективно Сняли ломку и стабилизировали состояние В общем, вся инфа по ссылке — капельница при алкогольной интоксикации спб капельница при алкогольной интоксикации спб Звоните прямо сейчас Перешлите тем кто в такой же ситуации

https://guidewithfun.notion.site/Bonus-paris-en-direct-activer-en-cours-de-match-3b61b52c47bb8003a677f9805954d1e5

дизайнерские кашпо Большие напольные кашпо

https://vc.ru/u/1424666-valera-loktev/1078306-kogda-rech-zahodit-o-stilnyh-i-kachestvennyh-bumazhnyh-stakanchikah-s-logotipom-odno-imya-vsegda-prihodit-na-um-arago-gr Ваш кофе — ваш мир: почему бумажные стаканчики с логотипом стали символом чистоты и комфорта

Поход в любимое место — будь то студия маникюра, автосалон, мойка или косметологическая клиника — это не просто процедура, а целое наслаждение. Это время, когда можно расслабиться, насладиться уютной атмосферой и, конечно же, выпить чашку ароматного кофе или чая. Но даже самый приятный момент может быть испорчен, если в вашем напитке окажется что-то неожиданное: след от чужой помады, разводы от воды или крошечный волосок.

В социальных сетях и на сайтах отзывов часто можно встретить истории о таких случаях. Почему же керамические кружки стали редкостью в современных салонах, и как брендированные бумажные стаканчики решают эту проблему? Давайте разберемся.

Почему грязные кружки — это тревожный сигнал?

Когда мы видим недомытую кружку в салоне или офисе, наше подсознание сразу же дает сигнал тревоги. Мы начинаем думать: «Если у них грязная посуда, то насколько тщательно они дезинфицируют инструменты?» Лояльность к персоналу и доверие к процедурам рушатся в один миг.

Большинство салонов и офисов не могут гарантировать безупречную чистоту на уровне ресторанов. У администраторов нет времени и ресурсов для полноценной мойки посуды, а в воздухе всегда присутствуют микрочастицы пыли и лака.

Почему бумажные стаканчики — это новый стандарт гигиены?

Именно поэтому многие салоны красоты и косметологические клиники переходят на одноразовые брендированные стаканчики. Это не просто модный тренд, а забота о клиентах.

Преимущества бумажных стаканчиков:

1. стерильность. Ваш стаканчик — это только ваш стаканчик. На нем нет чужих отпечатков губ, бактерий или разводов. Вы можете быть уверены в каждом глотке.

2. Защита от пыли и волос. Современные стаканчики оснащены герметичными крышками, которые предотвращают попадание волос и пыли в напиток.

3. Эстетика и стиль. Благодаря современным технологиям печати, салоны могут создавать на картонных стаканах настоящие шедевры. Мягкие цвета, стильные минималистичные дизайны и вдохновляющие надписи делают из простого стаканчика модный аксессуар.

Кофе как звезда Instagram

Мы все любим делиться моментами жизни в социальных сетях. Стильный стаканчик с логотипом салона — это идеальный фон для фотографий. Он превращает перерыв на кофе в вирусную рекламу. Девушки с восторгом фотографируют такие стаканчики, отмечают аккаунты салонов и рекомендуют их своим подругам.

Как выбрать идеальные стаканчики?

Не все бумажные стаканчики одинаково хороши. Дешевые варианты из супермаркета быстро размокают и обжигают пальцы. Профессионалы выбирают стаканы из качественного плотного картона с герметичными соединениями. Такие стаканы долго сохраняют температуру, не деформируются и не имеют посторонних запахов.

Итог:

В 2026 году забота о клиенте проявляется в мелочах. Если вы угощаете чаем в стильном одноразовом стакане с логотипом, это говорит о том, что здесь действительно заботятся о вашем комфорте и безопасности.

Хотите узнать больше о стильной упаковке для бьюти-индустрии, автосалона, офиса и подобрать идеальный вариант для своей студии? Посетите официальный сайт производственной компании «ARAGO group»

Москва, всем привет Близкий человек уже несколько дней в запое Дети напуганы В больницу тащить страшно Короче, только это реально спасло — вывод из запоя анонимно недорого с опытом Приехали через 40 минут В общем, вся инфа по ссылке — вывод из запоя наркология москва https://srochnyj.vyvod-iz-zapoya-na-domu-moskva.ru Не ждите пока станет хуже Перешлите тем кто в такой же ситуации

После первичной консультации пациент проходит обследование, позволяющее точно определить стадию зависимости и сопутствующие патологии. Используются лабораторные анализы, оценка неврологического статуса и сбор анамнеза. Уже на этом этапе начинается выстраивание контакта между пациентом и врачом, что особенно важно для доверия и готовности включиться в процесс.

Получить дополнительные сведения – http://narkologicheskaya-klinika-volgograd9.ru/chastnaya-narkologicheskaya-klinika-volgograd/

https://vk.ru/sochadler

https://webhitlist.com/profiles/blogs/limited-time-promotional-offers-for-everyone

В центре применяется последовательная модель лечения, включающая диагностику, детоксикацию, психотерапию, восстановление социальных навыков и постлечебное сопровождение. Такой подход даёт устойчивый эффект даже при тяжёлых формах зависимости.

Изучить вопрос глубже – http://narkologicheskaya-klinika-volgograd9.ru/lechenie-v-narkologicheskoj-klinike-volgograd/https://narkologicheskaya-klinika-volgograd9.ru

большие глиняные вазы печь для обжига керамики большая

https://lada-kazan.ru/remont-lada/brendirovannye-stakanchiki-kak-effektivnyj-marketingovyj-instrument Ваш кофе — ваш мир: почему бумажные стаканчики с логотипом стали символом чистоты и комфорта

Поход в любимое место — будь то студия маникюра, автосалон, мойка или косметологическая клиника — это не просто процедура, а целое наслаждение. Это время, когда можно расслабиться, насладиться уютной атмосферой и, конечно же, выпить чашку ароматного кофе или чая. Но даже самый приятный момент может быть испорчен, если в вашем напитке окажется что-то неожиданное: след от чужой помады, разводы от воды или крошечный волосок.

В социальных сетях и на сайтах отзывов часто можно встретить истории о таких случаях. Почему же керамические кружки стали редкостью в современных салонах, и как брендированные бумажные стаканчики решают эту проблему? Давайте разберемся.

Почему грязные кружки — это тревожный сигнал?

Когда мы видим недомытую кружку в салоне или офисе, наше подсознание сразу же дает сигнал тревоги. Мы начинаем думать: «Если у них грязная посуда, то насколько тщательно они дезинфицируют инструменты?» Лояльность к персоналу и доверие к процедурам рушатся в один миг.

Большинство салонов и офисов не могут гарантировать безупречную чистоту на уровне ресторанов. У администраторов нет времени и ресурсов для полноценной мойки посуды, а в воздухе всегда присутствуют микрочастицы пыли и лака.

Почему бумажные стаканчики — это новый стандарт гигиены?

Именно поэтому многие салоны красоты и косметологические клиники переходят на одноразовые брендированные стаканчики. Это не просто модный тренд, а забота о клиентах.

Преимущества бумажных стаканчиков:

1. стерильность. Ваш стаканчик — это только ваш стаканчик. На нем нет чужих отпечатков губ, бактерий или разводов. Вы можете быть уверены в каждом глотке.

2. Защита от пыли и волос. Современные стаканчики оснащены герметичными крышками, которые предотвращают попадание волос и пыли в напиток.

3. Эстетика и стиль. Благодаря современным технологиям печати, салоны могут создавать на картонных стаканах настоящие шедевры. Мягкие цвета, стильные минималистичные дизайны и вдохновляющие надписи делают из простого стаканчика модный аксессуар.

Кофе как звезда Instagram

Мы все любим делиться моментами жизни в социальных сетях. Стильный стаканчик с логотипом салона — это идеальный фон для фотографий. Он превращает перерыв на кофе в вирусную рекламу. Девушки с восторгом фотографируют такие стаканчики, отмечают аккаунты салонов и рекомендуют их своим подругам.

Как выбрать идеальные стаканчики?

Не все бумажные стаканчики одинаково хороши. Дешевые варианты из супермаркета быстро размокают и обжигают пальцы. Профессионалы выбирают стаканы из качественного плотного картона с герметичными соединениями. Такие стаканы долго сохраняют температуру, не деформируются и не имеют посторонних запахов.

Итог:

В 2026 году забота о клиенте проявляется в мелочах. Если вы угощаете чаем в стильном одноразовом стакане с логотипом, это говорит о том, что здесь действительно заботятся о вашем комфорте и безопасности.

Хотите узнать больше о стильной упаковке для бьюти-индустрии, автосалона, офиса и подобрать идеальный вариант для своей студии? Посетите официальный сайт производственной компании «ARAGO group»

Люди помогите советом Ситуация критическая Соседи стучат в стену Нужна срочная помощь на дому Короче, врачи приехали и поставили систему — вывод из запоя на дому срочно Приехали через 40 минут В общем, вся инфа по ссылке — вывод из запоя на дому москва круглосуточно https://srochnyj.vyvod-iz-zapoya-na-domu-moskva.ru Не ждите пока станет хуже Перешлите тем кто в такой же ситуации

Купить гидравлический насос шестеренный в Краснодаре Ищете оригинальные комплектующие мировых брендов? Предлагаем купить надежный гидронасос гидромотор НШ Bosch Rexroth в Краснодаре по доступным ценам. Оформите заказ на сертифицированную продукцию в несколько кликов.

https://www.edufex.com/forums/discussion/general/top-reasons-to-use-a-1xbet-bonus-code-when-registering

https://vk.ru/sochadler

https://xn—-7sbabaajcc4ffykc8aip2j.xn--p1ai/ne-tolko-napitok-kak-s-logotipom-stakan-uvelichivaet-doverie-pokupatelej-v-avtomobilnom-biznese-i-na-premium-mojkax/ Ваш кофе — ваш мир: почему бумажные стаканчики с логотипом стали символом чистоты и комфорта

Поход в любимое место — будь то студия маникюра, автосалон, мойка или косметологическая клиника — это не просто процедура, а целое наслаждение. Это время, когда можно расслабиться, насладиться уютной атмосферой и, конечно же, выпить чашку ароматного кофе или чая. Но даже самый приятный момент может быть испорчен, если в вашем напитке окажется что-то неожиданное: след от чужой помады, разводы от воды или крошечный волосок.

В социальных сетях и на сайтах отзывов часто можно встретить истории о таких случаях. Почему же керамические кружки стали редкостью в современных салонах, и как брендированные бумажные стаканчики решают эту проблему? Давайте разберемся.

Почему грязные кружки — это тревожный сигнал?

Когда мы видим недомытую кружку в салоне или офисе, наше подсознание сразу же дает сигнал тревоги. Мы начинаем думать: «Если у них грязная посуда, то насколько тщательно они дезинфицируют инструменты?» Лояльность к персоналу и доверие к процедурам рушатся в один миг.

Большинство салонов и офисов не могут гарантировать безупречную чистоту на уровне ресторанов. У администраторов нет времени и ресурсов для полноценной мойки посуды, а в воздухе всегда присутствуют микрочастицы пыли и лака.

Почему бумажные стаканчики — это новый стандарт гигиены?

Именно поэтому многие салоны красоты и косметологические клиники переходят на одноразовые брендированные стаканчики. Это не просто модный тренд, а забота о клиентах.

Преимущества бумажных стаканчиков:

1. стерильность. Ваш стаканчик — это только ваш стаканчик. На нем нет чужих отпечатков губ, бактерий или разводов. Вы можете быть уверены в каждом глотке.

2. Защита от пыли и волос. Современные стаканчики оснащены герметичными крышками, которые предотвращают попадание волос и пыли в напиток.

3. Эстетика и стиль. Благодаря современным технологиям печати, салоны могут создавать на картонных стаканах настоящие шедевры. Мягкие цвета, стильные минималистичные дизайны и вдохновляющие надписи делают из простого стаканчика модный аксессуар.

Кофе как звезда Instagram

Мы все любим делиться моментами жизни в социальных сетях. Стильный стаканчик с логотипом салона — это идеальный фон для фотографий. Он превращает перерыв на кофе в вирусную рекламу. Девушки с восторгом фотографируют такие стаканчики, отмечают аккаунты салонов и рекомендуют их своим подругам.

Как выбрать идеальные стаканчики?

Не все бумажные стаканчики одинаково хороши. Дешевые варианты из супермаркета быстро размокают и обжигают пальцы. Профессионалы выбирают стаканы из качественного плотного картона с герметичными соединениями. Такие стаканы долго сохраняют температуру, не деформируются и не имеют посторонних запахов.

Итог:

В 2026 году забота о клиенте проявляется в мелочах. Если вы угощаете чаем в стильном одноразовом стакане с логотипом, это говорит о том, что здесь действительно заботятся о вашем комфорте и безопасности.

Хотите узнать больше о стильной упаковке для бьюти-индустрии, автосалона, офиса и подобрать идеальный вариант для своей студии? Посетите официальный сайт производственной компании «ARAGO group»

ваза напольная высокая посуда из глины

https://подписать-сво-контракт.рф/

ebony teen porn

https://penzu.com/p/418d11ebd9a6dbf9

Москва, всем привет Ситуация критическая Соседи стучат в стену Таблетки не помогают Короче, только это реально спасло — вывод из запоя с выездом врача Через пару часов человек пришёл в себя В общем, не потеряйте контакты — вывод из запоя на дому москва вывод из запоя на дому москва Не ждите пока станет хуже Перешлите тем кто в такой же ситуации

Прописка в Москве остается важной темой для тех, кто планирует жить в столице постоянно или надолго. Наличие регистрации упрощает взаимодействие с различными службами, работодателями и учреждениями. Лучше заранее выбрать надежный способ оформления и проверить все детали – временная регистрация для иностранных граждан

https://pepper-pizza.ru/kofe-s-privkusom-chuzhoj-pomady-pochemu-bumazhnyj-stakan-v-salone-krasoty-stal-vernym-priznakom-vysokogo-klassa-i-chistoty/ Ваш кофе — ваш мир: почему бумажные стаканчики с логотипом стали символом чистоты и комфорта

Поход в любимое место — будь то студия маникюра, автосалон, мойка или косметологическая клиника — это не просто процедура, а целое наслаждение. Это время, когда можно расслабиться, насладиться уютной атмосферой и, конечно же, выпить чашку ароматного кофе или чая. Но даже самый приятный момент может быть испорчен, если в вашем напитке окажется что-то неожиданное: след от чужой помады, разводы от воды или крошечный волосок.

В социальных сетях и на сайтах отзывов часто можно встретить истории о таких случаях. Почему же керамические кружки стали редкостью в современных салонах, и как брендированные бумажные стаканчики решают эту проблему? Давайте разберемся.

Почему грязные кружки — это тревожный сигнал?

Когда мы видим недомытую кружку в салоне или офисе, наше подсознание сразу же дает сигнал тревоги. Мы начинаем думать: «Если у них грязная посуда, то насколько тщательно они дезинфицируют инструменты?» Лояльность к персоналу и доверие к процедурам рушатся в один миг.

Большинство салонов и офисов не могут гарантировать безупречную чистоту на уровне ресторанов. У администраторов нет времени и ресурсов для полноценной мойки посуды, а в воздухе всегда присутствуют микрочастицы пыли и лака.

Почему бумажные стаканчики — это новый стандарт гигиены?

Именно поэтому многие салоны красоты и косметологические клиники переходят на одноразовые брендированные стаканчики. Это не просто модный тренд, а забота о клиентах.

Преимущества бумажных стаканчиков:

1. стерильность. Ваш стаканчик — это только ваш стаканчик. На нем нет чужих отпечатков губ, бактерий или разводов. Вы можете быть уверены в каждом глотке.

2. Защита от пыли и волос. Современные стаканчики оснащены герметичными крышками, которые предотвращают попадание волос и пыли в напиток.

3. Эстетика и стиль. Благодаря современным технологиям печати, салоны могут создавать на картонных стаканах настоящие шедевры. Мягкие цвета, стильные минималистичные дизайны и вдохновляющие надписи делают из простого стаканчика модный аксессуар.

Кофе как звезда Instagram

Мы все любим делиться моментами жизни в социальных сетях. Стильный стаканчик с логотипом салона — это идеальный фон для фотографий. Он превращает перерыв на кофе в вирусную рекламу. Девушки с восторгом фотографируют такие стаканчики, отмечают аккаунты салонов и рекомендуют их своим подругам.

Как выбрать идеальные стаканчики?

Не все бумажные стаканчики одинаково хороши. Дешевые варианты из супермаркета быстро размокают и обжигают пальцы. Профессионалы выбирают стаканы из качественного плотного картона с герметичными соединениями. Такие стаканы долго сохраняют температуру, не деформируются и не имеют посторонних запахов.

Итог:

В 2026 году забота о клиенте проявляется в мелочах. Если вы угощаете чаем в стильном одноразовом стакане с логотипом, это говорит о том, что здесь действительно заботятся о вашем комфорте и безопасности.

Хотите узнать больше о стильной упаковке для бьюти-индустрии, автосалона, офиса и подобрать идеальный вариант для своей студии? Посетите официальный сайт производственной компании «ARAGO group»

https://vk.ru/sochadler

Слушайте кто знает Муж просто потерял себя Жена в истерике В больницу тащить страшно Короче, врачи приехали и поставили систему — вывод из запоя на дому срочно Поставили капельницу с детоксикационным раствором В общем, жмите чтобы сохранить — вывод из запоя недорого москва вывод из запоя недорого москва Не ждите пока станет хуже Перешлите тем кто в такой же ситуации

дизайнерские кашпо ваза напольная высокая

Здорова, народ Брат снова сорвался Соседи стучат в стену Нужна срочная помощь на дому Короче, врачи приехали и поставили систему — снятие интоксикации на дому быстро Сняли ломку и стабилизировали состояние В общем, телефон и цены тут — вывод из запоя на дому недорого вывод из запоя на дому недорого Звоните прямо сейчас Перешлите тем кто в такой же ситуации

Прокат лыж и сноубордов в Сочи позволяет гибко планировать катание. Можно взять снаряжение на один день, попробовать разные модели или подобрать комплект для всей поездки. Такой формат удобен для тех, кто ценит комфорт, мобильность и разумные расходы – Горнолыжный прокат в Адлере

Thanks for keeping things clear and to the point, that is honestly hard to find online these days, and after reading through electcateriarmccabe the message stayed consistent which makes me trust the information being shared more than I usually do on similar pages that cover this same kind of topic.

Reading more of the archives is now on my plan for the weekend, and a stop at progressmoveswithstructure confirmed the archive worth the time, the rare archive worth a dedicated reading session rather than just casual sampling is the rare archive of serious work and this site has clearly produced enough of that work to warrant the deeper exploration.

В этой статье мы рассматриваем разные способы борьбы с алкогольной зависимостью. Обсуждаются методы лечения, программы реабилитации и советы для поддержки близких. Читатели получат информацию о том, как преодолеть зависимость и добиться успешного выздоровления.

Как достичь результата? – как вывести из запоя самостоятельно

https://mygoodjob.ru/

Здорова, народ Брат снова сорвался Соседи стучат в стену Нужна срочная помощь на дому Короче, врачи приехали и поставили систему — вывод из запоя круглосуточно с выездом Приехали через 40 минут В общем, вся инфа по ссылке — вывод из запоя круглосуточно цены https://kodirovanie.vyvod-iz-zapoya-na-domu-moskva.ru Звоните прямо сейчас Перешлите тем кто в такой же ситуации

Здорова, народ Брат снова сорвался Соседи стучат в стену Нужна срочная помощь на дому Короче, врачи приехали и поставили систему — вывод из запоя дешево и качественно Приехали через 40 минут В общем, жмите чтобы сохранить — вывод из запоя дешево москва https://czena.vyvod-iz-zapoya-na-domu-moskva.ru Не ждите пока станет хуже Перешлите тем кто в такой же ситуации

При остром алкогольном отравлении появляются головокружение, рвота, сильная слабость, скачки давления, нарушение дыхания, обмороки и судороги. Это сигнал о том, что организм не справляется с интоксикацией, и без срочного медицинского вмешательства возможны опасные осложнения, вплоть до комы.

Изучить вопрос глубже – вызвать нарколога на дом

https://vk.ru/sochadler

Люди помогите советом Близкий человек уже несколько дней в запое Жена в истерике Таблетки не помогают Короче, врачи приехали и поставили систему — круглосуточный вывод из запоя без выходных Поставили капельницу с детоксикационным раствором В общем, жмите чтобы сохранить — вывод из запоя дешево москва https://czena.vyvod-iz-zapoya-na-domu-moskva.ru Не ждите пока станет хуже Перешлите тем кто в такой же ситуации

Москва, всем привет Отец не выходит из штопора Родственники не знают что делать Нужна срочная помощь на дому Короче, только это реально спасло — круглосуточный вывод из запоя без выходных Сняли ломку и стабилизировали состояние В общем, вся инфа по ссылке — цены на вывод из запоя на дому в москве цены на вывод из запоя на дому в москве Звоните прямо сейчас Перешлите тем кто в такой же ситуации

расшифровка анализов по фото онлайн расшифровка результатов анализов

Ben hier nu een maand of vier bezig en dacht ik gooi mijn ervaring er ook maar even in, want de meningen die je online vindt over lalabet casino review lezen als reclamefolders. Kwam er via iemand op een andere forum terecht en verwachtte er niet zo veel van.

Aan spellen geen gebrek — ergens rond de 3000+ dingen kun je draaien, al tel ik ze niet natuurlijk. Pragmatic domineert een beetje met Gates of Olympus en Sweet Bonanza, en zelf hang ik meer rond Play’n GO — Book of Dead blijft toch mijn vaste prik. NetEnt, Betsoft en wat Big Time Gaming titels vind je er ook, dus er valt genoeg te proberen.

Live gaat via Evolution en dat is gewoon prettig — de stream is stabiel, echte croupiers die ook gewoon Nederlands verstaan af en toe, en Crazy Time is daar natuurlijk de grote trekker. Dat kost me structureel geld, dat dan weer wel. Wie de actuele voorwaarden wil checken kan even kijken op https://lalabet-promocodes.nl/ voordat je stort, ze passen dat af en toe aan.

De welkomstbonus was bij mij 100% tot 500 euro plus 200 free spins, met een wagering van 35x — gewoon marktconform, meer niet. Je kunt al vanaf €10 storten, registreren was in een paar minuten geregeld. Wat me meeviel was hoe snel de KYC ging: paspoort geupload en binnen een dag goedgekeurd. Bij een ander casino wachtte ik ooit een week.

Mijn uitbetalingen gaan via Neteller en binnen een dag heb ik het binnen. Visa en Mastercard werken ook, maar dan wacht je wel drie werkdagen. Crypto kan ook, ik heb een keer met Bitcoin getest en dat was de snelste van allemaal. Het irritante puntje: support liet me een keer twintig minuten wachten, en ze antwoordden eerst in het Engels. Het kwam wel goed, maar goed.

Mobiel gaat via de browser, geen app nodig en dat laadt snel genoeg. Waar het in Nederland altijd over gaat is de vergunning — ze draaien op Curacao, geen KSA-vergunning, en dat moet je gewoon voor jezelf afwegen. Ik heb nooit gedoe gehad met uitbetalingen, maar dat is een ervaring, van mij.

Москва, всем привет Брат снова сорвался Жена в истерике Нужна срочная помощь на дому Короче, врачи приехали и поставили систему — вывод из запоя на дому круглосуточно анонимно Приехали через 40 минут В общем, вся инфа по ссылке — вывод из запоя с выездом на дом https://czena.vyvod-iz-zapoya-na-domu-moskva.ru Звоните прямо сейчас Перешлите тем кто в такой же ситуации

Москва, всем привет Отец не выходит из штопора Жена в истерике Нужна срочная помощь на дому Короче, единственное что вытащило из запоя — вывод из запоя на дому цена доступная Сняли ломку и стабилизировали состояние В общем, телефон и цены тут — вывод из запоя дешево вывод из запоя дешево Вывод из запоя на дому — это реальный выход Перешлите тем кто в такой же ситуации

https://vk.ru/sochadler

расшифровка анализа крови бесплатно расшифровка результатов анализов бесплатно

Архив эротических рассказов. Горячие истории о сексе, желании и наслаждении для взрослых. Читайте бесплатно, новые рассказы каждый день. Откройте тайны страсти, фантазии и яркие эмоции https://eroxtales.top/

Здорова, народ Ситуация критическая Родственники не знают что делать В больницу тащить страшно Короче, врачи приехали и поставили систему — вывод из запоя на дому цена доступная Сняли ломку и стабилизировали состояние В общем, не потеряйте контакты — срочный вывод из запоя в москве https://czena.vyvod-iz-zapoya-na-domu-moskva.ru Звоните прямо сейчас Перешлите тем кто в такой же ситуации

Слушайте кто знает Отец не выходит из штопора Родственники не знают что делать Нужна срочная помощь на дому Короче, единственное что вытащило из запоя — вывод из запоя круглосуточно с выездом Поставили капельницу с детоксикационным раствором В общем, вся инфа по ссылке — вывод из запоя на дому клиника https://lechenie.vyvod-iz-zapoya-na-domu-moskva.ru Не ждите пока станет хуже Перешлите тем кто в такой же ситуации

В этой статье мы обсудим процесс восстановления после зависимостей, акцентируя внимание на различных методах и подходах к реабилитации. Читатели узнают, как создать план выздоровления и использовать полезные ресурсы для достижения устойчивых изменений.

Рассмотреть проблему всесторонне – профилактика заболевания алкоголизма

создай свою музыку Мечтаете записать трек для важного события? Нейросети помогут создать идеальную песню под ваше настроение и тему. Попробуйте сгенерировать музыку онлайн!

Люди помогите советом Ситуация критическая Дети напуганы Таблетки не помогают Короче, врачи приехали и поставили систему — вывод из запоя на дому круглосуточно анонимно Через пару часов человек пришёл в себя В общем, телефон и цены тут — вывод из запоя недорого в москве https://narkolog.vyvod-iz-zapoya-na-domu-moskva.ru Вывод из запоя на дому — это реальный выход Перешлите тем кто в такой же ситуации

При остром алкогольном отравлении появляются головокружение, рвота, сильная слабость, скачки давления, нарушение дыхания, обмороки и судороги. Это сигнал о том, что организм не справляется с интоксикацией, и без срочного медицинского вмешательства возможны опасные осложнения, вплоть до комы.

Исследовать вопрос подробнее – https://narcolog-na-dom-novokuznetsk00.ru/narkolog-na-dom-czena-novokuzneczk/

Bez owijania w bawelne, gram tam od jakiegos kwartalu i dopiero po czasie mam wyrobione zdanie. Znalazlem to przypadkiem, przegladajac kasyna online ranking, bo mnie zmeczyly miejsca gdzie weryfikacja trwa wieki.

Katalog jest gruby — jakies 2000 z hakiem automatow, choc jak zwykle wiekszosc klika sie raz i zapomina. Pragmatic Play jest najbardziej widoczny, Gates of Olympus i Book of Dead stoja na froncie, dorzucili Yggdrasil, Betsoft i Microgaming. Na zywo jedzie Evolution, kilka stolow jest po polsku, a Lightning Roulette i Crazy Time zawsze ma tlum.

Pakiet na start to doplata 100% do 2000 zl i darmowe spiny, warunek obrotu to x35 — uczciwie, choc bez fajerwerkow. Bywa drobny no deposit za weryfikacje numeru, choc wielkich pieniedzy z tego nie ma. Kody sie zmieniaja, wiec zerknac na aktualna liste na https://searchengines.guru/ru/users/2246526 przed rejestracja.

Sam start poszla szybko, minimalny depozyt 40 zl bez przesady. Place przez Przelewy24, bo z BLIK-iem to najszybsza droga, ale sa tez karty, Skrill, Neteller, jest i Bitcoin dla chetnych. Pierwszy cashout zeszla prawie dobe, bo weryfikacja, nastepne schodza tego samego dnia.

Minus, ktory musze wypisac — support po polsku bywa tylko wieczorem, a bot na starcie potrafi zajechac cierpliwosc. Aplikacja nie zachwyca, choc na telefonie wszystko chodzi plynnie. Licencja Curacao — nie jest to top tier, natomiast wyplaty realizuja i tyle mi wystarczy. Ktos pytal wyzej o inne budy, typu nv casino czy jest bezpieczne — tam nie zagladalem, wiec sie nie wypowiem.

Слушайте кто знает Близкий человек уже несколько дней в запое Жена в истерике Нужна срочная помощь на дому Короче, единственное что вытащило из запоя — вывод из запоя на дому цена доступная Сняли ломку и стабилизировали состояние В общем, не потеряйте контакты — вывод из запоя круглосуточно в москве https://lechenie.vyvod-iz-zapoya-na-domu-moskva.ru Вывод из запоя на дому — это реальный выход Перешлите тем кто в такой же ситуации

клиника лечения спины и суставов в пушкино травматолог пушкино

Дренажный напиток От отеков ног страдают многие, особенно после долгих часов на ногах или сидячей работы. Специальные дренажные напитки улучшают микроциркуляцию и снимают усталость в нижних конечностях. Почувствуйте приятную легкость и забудьте о дискомфорте к концу дня.

Здорова, народ Отец не выходит из штопора Родственники не знают что делать В больницу тащить страшно Короче, врачи приехали и поставили систему — снятие интоксикации на дому быстро Поставили капельницу с детоксикационным раствором В общем, телефон и цены тут — вывод из запоя на дому москва вывод из запоя на дому москва Не ждите пока станет хуже Перешлите тем кто в такой же ситуации

торт для мужчины торт для мужчины

Эти действия помогают быстро восстановить водно-электролитный баланс и снизить нагрузку на внутренние органы. После проведения процедур врач дает рекомендации по дальнейшему наблюдению и реабилитации.

Узнать больше – https://narcolog-na-dom-kaliningrad00.ru/

Obstawiam tu od jakichs czterech miesiecy i nie ukrywam trafilem tu przypadkiem. Wczesniej siedzialem na dwoch innych budkach i glownie chodzilo mi o to, zeby moc obstawiac z telefonu w tramwaju. No i tutaj mostbet aplikacja daje rade — chodzi plynnie nawet na moim starym Xiaomi.

Wybor jest absurdalny, cos kolo 2-3 tysiecy pozycji i wiekszosc to normalni dostawcy. Play’n GO dominuje — Sweet Bonanza leci u mnie codziennie, choc od jakiegos czasu bardziej klikam Betsoft. Live jest od Evolution, prawdziwi krupierzy, nie zadne automaty, Lightning Roulette potrafi wciagnac na godzine. Po polsku stolu niestety nie ma i to mi troche przeszkadza.

Bonus powitalny jest w okolicach 100% do jakichs 1400 zl plus 250 free spinow, rozbite na kilka dni. Obrot to x60 na spinach — realne, ale trzeba miec cierpliwosc. Szczegoly promocji sa opisane na mostbet app download jesli chcesz to dokladnie przeliczyc. Minimalny depozyt zaczyna sie od 20 zl, zapis to dwie minuty, weryfikacja dokumentow poszla w jedna dobe.

Wyplacam najczesciej na Skrill i schodzi to do 2-3 godzin. Na Mastercard trwalo dluzej — dwa dni robocze. Bitcoina i USDT tez przyjmuja, ale tego nie testowalem. Co mi sie nie spodobalo to weryfikacja przy pierwszej wyplacie — niby standard, a irytuje.

Support odpowiada po polsku, chociaz o drugiej w nocy odpowiadali mi po angielsku. Czekalem jakies 4 minuty, bez kopiuj-wklej regulaminu. Curacao — jak wiekszosc takich miejsc, nie jest to nic pod polskim nadzorem — kazdy niech sobie sam to przemysli.

Plik apk pobiera sie bezposrednio ze strony, nie ma tego w sklepie Play. Trzeba pozwolic na zrodla zewnetrzne — dla niektorych to bariera, dla mnie zaden problem. Na iOS jest osobny sposob instalacji. Push-e potrafia zasypac, wylaczylem to drugiego dnia.

Obstawiam tu od mniej wiecej pol roku i szczerze mowiac zapisalem sie po nudnym wieczorze. Przedtem gralem gdzie indziej i glownie chodzilo mi o to, zeby moc obstawiac z telefonu w tramwaju. No i tutaj mostbet aplikacja daje rade — nie tnie nawet na moim zajechanym Samsungu.

Automatow jest tam z 3000+ i w wiekszosci znane studia. Pragmatic Play dominuje — Gates of Olympus to moj standard, choc ostatnio czesciej klikam Yggdrasilu. Live jest od Evolution, prawdziwi krupierzy, nie zadne automaty, Crazy Time jest tam oczywiscie. Polskiego stolu jednak nie znalazlem i na to troche narzekam.

Pakiet na start to 100% do jakichs 1400 zl i do tego okolo 250 spinow, nie wszystkie naraz — po 50 dziennie. Obrot jest x60, wiec bez cudow — niski to on nie jest, uczciwie mowiac. Szczegoly promocji sa opisane na mostbet app polska jesli chcesz to dokladnie przeliczyc. Wplata minimalna to jakies 20 zl, rejestracja zajela mi doslownie minute, dokumenty zatwierdzili po niecalej dobie.

Wyplacam zazwyczaj na e-portfel i jest w miare ekspresowo. Karta czekalem dwa dni. BTC obsluguja, ale tego nie testowalem. Co mi sie nie spodobalo to zamrozenie wyplaty na czas KYC — logiczne, tylko po co to na ostatnia chwile.

Obsluga po polsku dziala, chociaz o drugiej w nocy odpowiadali mi po angielsku. Odpisuja w kilka minut, bez kopiuj-wklej regulaminu. Dzialaja na licencji Curacao, wiec bez polskiego pozwolenia — to trzeba wiedziec zawczasu.

Apke sciagalem z ich strony, bo w Google Play tego nie znajdziesz. Trzeba odblokowac instalacje z nieznanych zrodel — standard, nic dziwnego. Wersja pod iOS tez jest, kolega ma. Push-e potrafia zasypac, wylaczylem to drugiego dnia.

медицинский центр пушкино клиника лечения спины и суставов в пушкино

Катанка стальная купить в Ташкенте. Компания MODULSTAL поставляет стальную катанку, применяемую при производстве проволоки, крепежных изделий, сварочных материалов и армирующих конструкций. Вся продукция соответствует стандартам качества и доступна со склада в Ташкенте.

Люди подскажите Отец не выходит из штопора Родственники не знают что делать Таблетки не помогают Короче, врачи приехали и поставили систему — вывод из запоя цена на дому фиксированная Через пару часов человек пришёл в себя В общем, не потеряйте контакты — вывод из запоя на дому в москве https://lechenie.vyvod-iz-zapoya-na-domu-moskva.ru Не ждите пока станет хуже Перешлите тем кто в такой же ситуации

Горнолыжный прокат Красной Поляны востребован у гостей курорта, которые хотят быстро выйти на трассу и не тратить время на покупку экипировки. Подбор лыж, сноубордов и ботинок помогает кататься комфортнее, а разные варианты снаряжения подходят под разные уровни подготовки: Горнолыжный прокат в Адлере

торт на свадьбу торт на день рождения

Слушайте кто сталкивался Брат снова сорвался Дети напуганы Таблетки не помогают Короче, единственное что вытащило из запоя — вывод из запоя цена на дому фиксированная Поставили капельницу с детоксикационным раствором В общем, телефон и цены тут — вывод из запоя с выездом москва вывод из запоя с выездом москва Звоните прямо сейчас Перешлите тем кто в такой же ситуации

Этот обзор посвящен успешным стратегиям избавления от зависимости, включая реальные примеры и советы. Мы разоблачим мифы и предоставим читателям достоверную информацию о различных подходах. Получите опыт многообразия методов и найдите подходящий способ для себя!

Практические советы ждут тебя – после кофе можно алкоголь

сюрвейер сюрвейерские услуги

Эти действия помогают быстро восстановить водно-электролитный баланс и снизить нагрузку на внутренние органы. После проведения процедур врач дает рекомендации по дальнейшему наблюдению и реабилитации.

Подробнее тут – http://narcolog-na-dom-kaliningrad00.ru/

клиника лечения спины и суставов в пушкино медицинский центр пушкино

Средство от отеков От отеков ног страдают многие, особенно после долгих часов на ногах или сидячей работы. Специальные дренажные напитки улучшают микроциркуляцию и снимают усталость в нижних конечностях. Почувствуйте приятную легкость и забудьте о дискомфорте к концу дня.

В этой статье мы рассматриваем разные способы борьбы с алкогольной зависимостью. Обсуждаются методы лечения, программы реабилитации и советы для поддержки близких. Читатели получат информацию о том, как преодолеть зависимость и добиться успешного выздоровления.

Подробнее – https://stop-alko.info/alkogolizm/rossiyskie-zvezdyalkogoliki.html

взять займ онлайн срочно займы онлайн

Люди подскажите Отец не выходит из штопора Соседи стучат в стену В больницу тащить страшно Короче, врачи приехали и поставили систему — вывод из запоя анонимно недорого с опытом Приехали через 40 минут В общем, жмите чтобы сохранить — выведение из запоя в москве https://lechenie.vyvod-iz-zapoya-na-domu-moskva.ru Не ждите пока станет хуже Перешлите тем кто в такой же ситуации

Здорова, народ Близкий человек уже несколько дней в запое Соседи стучат в стену Нужна срочная помощь на дому Короче, врачи приехали и поставили систему — снятие интоксикации на дому быстро Приехали через 40 минут В общем, вся инфа по ссылке — вывод из запоя на дому круглосуточно вывод из запоя на дому круглосуточно Вывод из запоя на дому — это реальный выход Перешлите тем кто в такой же ситуации

торт на заказ торт на день рождения

Слушайте кто страховку ищет Менеджеры впаривают лишние услуги А в итоге всё равно переплатил Короче, быстро и без лишней головной боли — оформить осаго на автомобиль онлайн с кэшбэком Сэкономил почти 4000 рублей В общем, вся инфа вот здесь — купить осаго цены https://strahovka-msk.ru Не тратьте время в офисах Перешлите тому у кого машина

Прокат лыж Красная Поляна помогает быстро подобрать комплект для трасс разного уровня. Правильно выбранные лыжи и ботинки делают катание комфортнее, а возможность аренды позволяет не вкладываться в собственное снаряжение. Такой вариант выбирают многие гости курорта – Пункт прокат лыж в Красной Поляне

Премиальные и бизнес-класс новостройки Москвы позволяют подобрать квартиру в доме с современными стандартами комфорта. Внимание уделяется архитектуре, лобби, дворам, инженерии, безопасности и сервисам. Такой подход делает жилой комплекс более удобным для ежедневной жизни, 26 Парквью

Квартиры в элитных ЖК Москвы ценятся за удачные локации, качественные материалы, современную архитектуру и продуманную инфраструктуру. Новостройки бизнес-класса позволяют жить в комфортной среде, где каждый элемент пространства работает на удобство владельца – https://mr-elit.ru/

клиника лечения спины и суставов в пушкино медицинский центр пушкино